Defining “Bubble”

Much of today’s debate depends on how one defines a bubble. To paraphrase Benjamin Graham, a bubble occurs when market prices detach significantly from intrinsic value and are driven by emotion, herd behavior, and speculation rather than fundamentals. When a bubble bursts, prices tend to retreat toward underlying value — not because the technology was worthless, but because the market overshot its plausible valuation.

There are two types of bubbles worth distinguishing:

1. Timing / Structural Bubbles

These occur when real value exists but is expected to materialize sooner than it realistically can. Examples include:

Dot-com (late 1990s–2000): Many Internet companies traded at absurd multiples. In 2000, the average revenue multiple for IPOs was ~48.9. [1] Even giants like Cisco took years to surpass their peak valuations (which only happened late 2025). Pets.com tried to be what Chewy is. Webvan tried to be what Instacart is. DoorDash achieved the vision that Kosmo.com was unable to attain. Others, like Amazon and NVIDIA, sustained the downturn and became some of the largest companies in the world.

Automobiles (early 1900s): 3,300 companies manufactured autos between 1900 and 1925. [2] By 1929, only 44 remained, and the big 3 (GM, Chrysler, Ford) controlled 80% of the market. Once the market was saturated, supply expansion led to increased price competition. As a result, manufacturers and dealers provided more attractive financing options like installments, lower down-payment requirements, and extended term loans. Autos changed from a cash to credit purchase.

Railroads (1840s UK): Rail was a transformative technology for moving goods, but capital was deployed faster than utilization could grow. This led to collapses followed by decades of economic benefit. New capital was brought into the market through growth in a press ecosystem. It highlighted financial speculation, a growing middle class with savings to invest, and joint-stock company structures that enabled widespread equity ownership. Rail became one of the first mass retail equity manias. Installment payments were popularized, enabling investors to invest minimal amounts up front and the remainder through later capital calls. A mindset of selling before full payment was due spread through the investment community, thus creating a market in which builders stopped assessing the feasibility of a rail and instead fulfilled demand from those who wanted to flip the asset. Ultimately, investors were required to pay remaining installments with liquidity they did not have. This led to distressed selling while asset prices rapidly declined, interest rates increased, and speculative capital dried up. Rail share prices sank approximately 2/3 from the peak [3] and new investment was non-existent. Those rail assets provided significant GDP growth to England, though it took many years for investors to realize a profit.

The Housing Crash of the Global Financial Crisis (“GFC”): Similar to rail, new financing mechanisms enabled more investors – mostly unsophisticated – to enter the market. Set aside the mortgage fraud committed during this time and instead think about interest-only loans, ARMs, piggyback loans, teaser rates, etc. These enabled a flip mentality and allowed those without capital to enter the market. Housing had a mantra that “nationwide, housing prices never fall,” which had been generally accurate. During the 2001 recession, interest rates were reduced to historically low levels. Lenders packaged and securitized loans, reducing the incentive to rigorously approve buyers. Not to mention, they were able to offload that securitized risk to Fannie and Freddie. Non-bank lenders entered the market. Risk became systemic and widely underestimated, leading to insolvency of some historic financial institutions. Housing starts far exceeded population growth and were driven by capital instead of occupancy. Owning became significantly more expensive than renting and so, the bubble popped.

These markets were not devoid of value — but the timing of expansion and monetization was overly optimistic.

2. Fad / Pure Speculative Bubbles

These lack fundamental value and are mostly sustained by optimism alone.

- Tulip Mania of the 1630s: The classic example is the Tulip Mania of the 1630s, where bulb prices reached more than ten times the annual income of a skilled worker. [4] A phenomenon so shocking that it remains the gold standard of what a bubble is. The greatest factor was scarcity – considering tulips’ 7-year growth cycle from seed to bulb. This was during a time of great prosperity in Holland and was primarily confined to those seeking luxury goods. This market was fueled by unsophisticated investors hoping to get rich quick.

- NFT Boom of 2021-2022: While there may be economic utility in future NFTs, this era of assets was detached from fundamentals. Trading volumes have since collapsed ~97%. [5] At its peak, a Bored Ape sold for ~$24 million in late 2021. According to CoinGecko, recent sales land somewhere between $10-$15k. The pattern repeats – a market characterized by unsophisticated investors rapidly piling in – fueled by an expansion of capital from stimulus funds, savings from COVID lockdowns, and most importantly, 0% interest rates. Money was essentially free, people were bored from a lack of social stimulus, and new capital was looking for a speculative home.

Historical Patterns of Bubbles

From railroads to housing to tech, we observe common elements:

-

New, unsophisticated capital enters the market

-

Prices rise in momentum rather than earnings or cash flows

-

The “this time is different” narratives

-

Credit expands, enabling easier capital inflows

-

Asset supply outpaces underlying demand

AI: Under the Bubble Microscope

Let’s walk through the criteria, grounded in current data, one by one:

1. Is the Market Pulling in New Investors?

In public markets, retail participation in AI themes has certainly grown as part of the broader tech rally — particularly among ETFs and large tech names. In private markets, however, barriers persist:

-

-

Retail investors generally cannot access early-stage AI venture deals (SPVs, etc.).

-

-

-

Private allocations are dominated by institutions, family offices, and accredited investors.

-

Conclusion: New investors are participating, especially in derivatives and public equities, but private allocations remain gated – therefore, allocation to venture has not meaningfully increased.

2. Are Prices Driven by Momentum Rather Than Fundamentals?

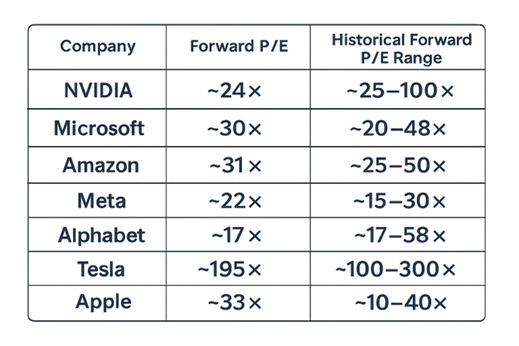

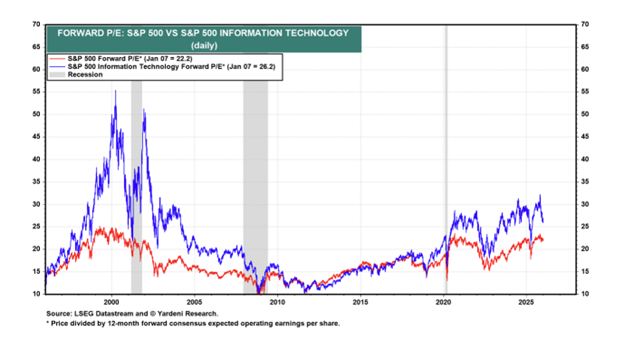

Some AI valuations clearly reflect momentum and expectations. For example, the MAG7 has seen outsized performance: Taken together, these names now represent ~32.6% of the S&P 500 by market cap. [6] The overall S&P 500 trades at ~21.9× forward earnings — above its 10-year average of 18.6×. [6]

Taken together, these names now represent ~32.6% of the S&P 500 by market cap. [6] The overall S&P 500 trades at ~21.9× forward earnings — above its 10-year average of 18.6×. [6]

While broad equities are relatively expensive by historical standards, valuations within this range are not extreme given secular growth trajectories. Multiple compression remains a risk, but these valuations do not scream irrational without deeper sector context.

Since most private companies aren’t typically valued on a PE ratio, it’s important to look at sales and users to forecast an ability to either grow or monetize said users. ChatGPT reached 100 million users in 2 months. Previously, Facebook held the record – hitting 100 million users at the 4.5 year mark. Lovable hit a revenue run rate of $100mm in just 8 months, Cursor reached a revenue run rate of $100mm with fewer than 20 employees, and Claude Code hit a $1B revenue run rate in just 5 months. This is growth unlike anything we have ever seen

3. “This Time Is Different” Syndrome

There’s no shortage of bold claims about AI’s transformative work on everything from autonomous vehicles to robotics to enterprise workflows. However:

- We are not inventing new valuation mathematics (e.g., eyeballs, clicks).

- We are seeing tangible revenue growth today from AI products.

Several signals point to real economic activity:

Productivity Gains: According to Fullview, employees using AI report an average 40% productivity boost, with controlled studies showing 25–55% improvements depending on the function. Federal Reserve research found workers using generative AI saved 5.4% of their work hours weekly, with frequent users saving over 9 hours per week.

Revenue Growth / Client Commitments: As of 2025, 78% of organizations now use AI in at least one business function. That’s a 42% increase since 2023. Fullview Enterprise generative AI spending hit $37 billion in 2025, up 3.2x year-over-year from $11.5 billion in 2024, with more than half of that flowing to the application layer — meaning companies are buying solutions, not just building experiments. Menlo Ventures

Productivity: In 2025, 31% of enterprise AI use cases reached full production — double the figure from 2024. ISG These tools take time and money to deploy and configure, as well as training humans to reconfigure their work routines before ROI is realized, but what is significant is that there is real infrastructure being developed. Organizations increased spending on AI compute and storage infrastructure by 166% year-over-year in Q2 2025 alone, reaching $82 billion in a single quarter. IDC projects the global AI infrastructure market will reach $758 billion annually by 2029.

The narrative isn’t naive magic — enterprise adoption is real, though timing and monetization trajectories vary widely.

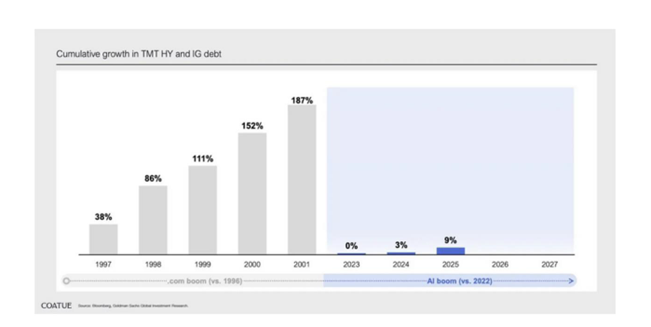

4. Expansion of Credit – Private and Public

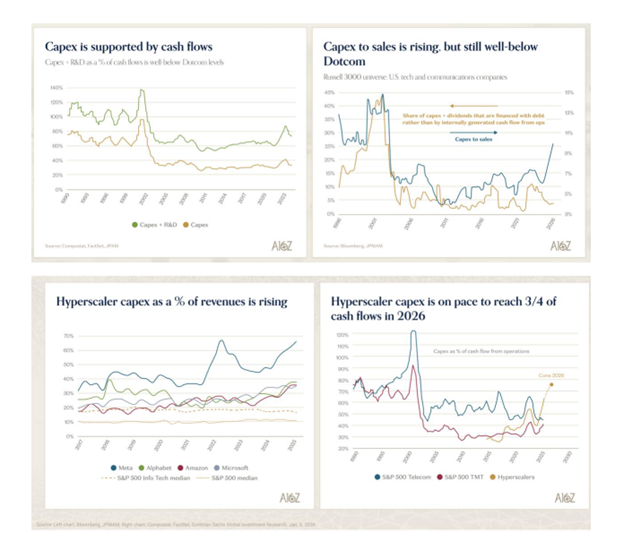

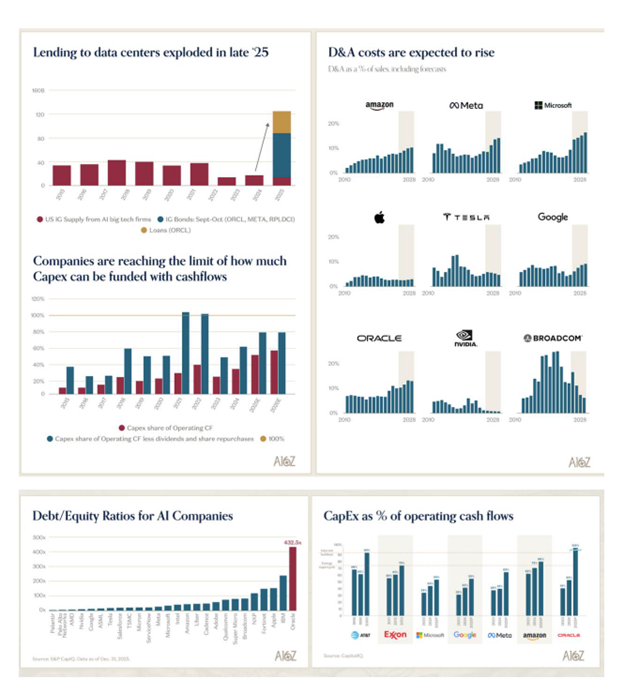

One of the strongest similarities between the AI cycle and past bubbles is credit expansion, especially that outside of traditional VC funding:

- Private credit has surged as an alternative capital source for AI infrastructure, particularly for data center construction and hardware capex. According to industry coverage, Big AI data center deals from Oracle and peers have been financed significantly through debt, rather than cash flow alone. [7]

- Data center capex from hyperscalers are also expanding dramatically. Analysts estimate ~$400B invested in 2025, rising to ~$600B+ projected in 2026 in cloud and AI infrastructure buildouts. [7]

This is distinct from the ZIRP era, though debt remains a critical piece of the AI funding puzzle.

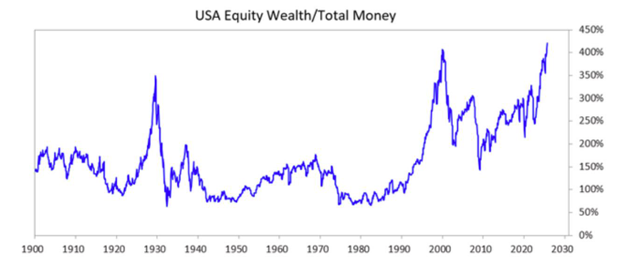

Ray Dalio analyzed the difference between wealth and money – and now, more than ever, there is a significant amount of wealth vs. money. It’s true that financial wealth can be created more easily than money, but to turn that wealth into money, something has to give – an asset must be sold. Dalio believes that this is what causes bubbles to burst.

He provides the chart below:

If demand growth slows meaningfully, this is where we could see forced selling and a pullback in asset prices. It’s a critical data point to watch, though this capex is still meaningfully below that of the dot-com era.

5. Uncertainty Around Timing of Cash Flows

We’ve identified that AI creates real revenue, but monetization timing and scale remain uncertain:

- Enterprises may slow purchasing in downturns

- Consumers may opt for lower-cost alternatives

- Revenue recognition for AI platforms often lags adoption

Even with real demand, forecasting cash flows is a challenge that contributes to valuation uncertainty – though, we see many examples of private AI companies beating growth expectations. The market has underestimated the timing of cash flows but it’s quite possible that at some point the outlook becomes too optimistic.

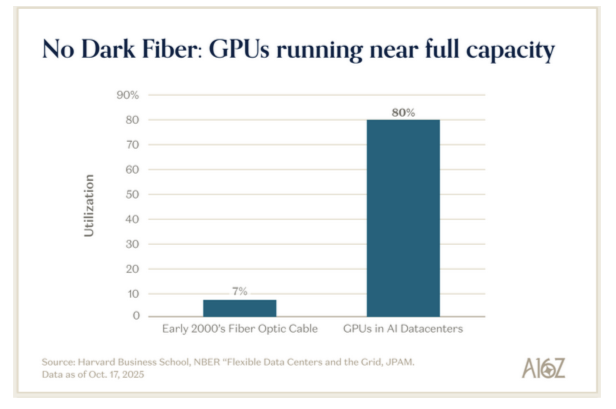

6. Supply vs. Demand Imbalances

Unlike telecom during the dot-com era, where less than 10% of capacity was used after buildout, AI compute capacity is consumed rapidly once available. [8] The critical shortage today is GPUs and AI accelerators, not unused capacity.

This suggests that, at least at the infrastructure layer, supply has not outpaced demand.

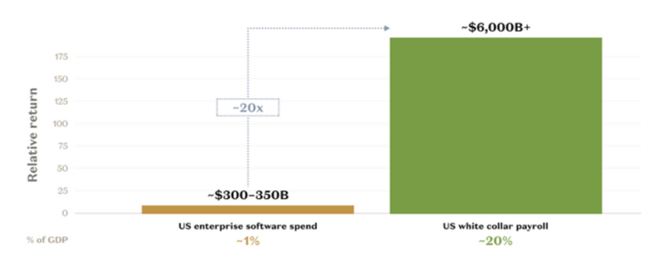

Sizing the Opportunity, Not the Hype

Let’s contextualize the market opportunity in economic terms:

- There are roughly 48 million software developers globally, with typical compensation around ~$71k. [9]

- There are an estimated ~20 million call center support roles worldwide, averaging ~$27k. [10]

Even conservative capture of value with no market expansion (say 10% share of those markets through AI adoption) implies a total addressable opportunity of approximately $394B (coding + customer service). This is equal to nearly 20 median S&P 500 companies’ revenues. [11] It’s flawed math, but it does highlight how large the market for labor replacement and enhancement is. When you begin to add layers: law, finance, marketing, sales, etc. – you get a sense for just how massive of an economic opportunity this is.

According to A16Z, today’s top 50 private AI companies are generating over $40B of revenue run rate.

The labor replacement market for AI is massive. Lightspeed estimates that this market will be a $19.9T market by 2030. Regardless of who’s estimate you trust, it’s undeniable that this market is significantly larger than enterprise software.

So, Is There a Bubble?

Yes — at the Micro Level. There are clearly bubble-like phenomena in AI:

- Rich valuations for some private companies

- Speculative capital chasing “winner-take-all” narratives

- Founder valuations unconnected to near-term revenue

At the macro level, the proposition that AI represents lasting economic value is credible:

- Real revenues exist today

- Enterprise capex and AI spend are material and growing

- Public equities and credit markets are allocating capital at disciplined multiples

In market cycles, technology adoption often looks like a bubble at the crest – even if the underlying technology is fundamentally transformative.

Conclusion

AI isn’t a fad like tulips. It isn’t purely speculative like some parts of the NFT market. But it does exhibit localized speculative dynamics around certain companies and valuations.

At a macro scale, we are investing against real economic value creation with measurable revenue opportunities that dwarf traditional industry metrics.

Make no mistake, some companies will fail. Some valuations will compress. Some capital will be lost.

That’s not a burst bubble. It’s competition and technological evolution at scale. At this stage of the cycle, the most rational strategy for long-term investors is broad participation rather than precision timing. While AI will undoubtedly produce a handful of generational companies, just as the internet era produced Amazon, Google, and Salesforce, the distribution of outcomes will likely be extraordinarily uneven. Capital will chase thousands of startups, but only a small percentage will compound into category-defining winners.

A fund-of-funds model materially increases the possibility of owning those outliers by diversifying across managers, stages, geographies, and technical theses. Instead of making concentrated bets in a market where technological and competitive curves are moving faster than any single investor can track, a diversified portfolio provides exposure to a larger opportunity set. This casts a wider net, potentially wrapping arms around the companies and founders that will ultimately reshape industries. In periods of technological discontinuity, breadth can become a superpower. It can capture upside from breakthroughs while insulating portfolios from inevitable failures along the way.

And so, the bubble floats.

Citations

[1] “Blog Study,” The Times. IPO revenue multiple ~48.9× in 2000

[2] “Automobile History.” History.com, 27 Feb. 2025, https://www.history.com/articles/automobiles

[3] Odlyzko, Andrew. “The Collapse of the Railway Mania…” 25 Jun. 2011 https://www-users.cse.umn.edu/~odlyzko/doc/mania02.pdf

[4] Hayes, Adam. “Tulipmania…”16 Mar. 2026, Tulipmania: About the Dutch Tulip Bulb Market Bubble

[5] NFT volume collapse ~97%

[6] Daly, Lyle. “The Magnificent Seven’s…” The Motley Foo.18 Mar. 2026, The Magnificent Seven’s Market Cap vs. the S&P 500 | The Motley Fool

[7] Trendonify. Feb 2026, S&P 500 PE Ratio

[8] Channel Futures — Big AI data center debt deals

[9] Elias, Jennifer. “Tech AI spending…” CNBC. 6 Feb. 2026, Tech AI spending approaches $700 billion in 2026, cash taking big hit

[10] AI supply vs. demand refers to the use of artificial intelligence to analyze and predict supply and demand dynamics within various sectors.

[11] “47.2 Million Developers.” SlashData. 8 May. 2025, https://www.slashdata.co/post/global-developer-population-trends-2025-how-many-developers-are-there

Disclaimer: Top Tier Capital Partners, LLC (“TTCP”) provides this material for general educational and informational purposes only. It does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or to purchase, shares, units or other interests in any security or investment and must not be construed as investment or financial advice. TTCP has not considered any reader’s financial situation, objective or needs in providing this information.

The value of any investment including, but not limited to, a venture investment may fall as well as rise and you may not get back your original investment. Past performance is not necessarily a guide to future performance or returns. Certain information contained herein has been obtained from third-party sources. While such sources are believed to be reliable, TTCP has not independently verified such information and makes no representation or warranty as to its accuracy or completeness. TTCP disclaims any liability arising from the use of such information and TTCP undertakes no (and disclaims any) obligation to update, modify or amend this document or to otherwise notify you in the event that any matter stated in the materials, or any opinion, projection, forecast or estimate set forth in the document, changes or subsequently becomes inaccurate. This material is intended only for the direct recipients to whom it was sent. Any distribution, reproduction or other use of this presentation by recipients is strictly prohibited.

The commentary regarding artificial intelligence (“AI”) reflects TTCP’s current market observations and views based on information available at the time of writing. The future development, adoption, and economic impact of AI technologies are inherently uncertain. Market conditions associated with emerging technologies can change rapidly, and there can be no assurance that current trends or valuations related to AI will continue.

TTCP is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). Registration of an investment adviser with the SEC does not imply any level of skill or training. For additional information regarding TTCP, please see TTCP’s Form ADV which can be found on the SEC’s web site (www.sec.gov).

Copyright © 2026 Top Tier Capital Partners, LLC All rights reserved.

2026-019